In our previous articles, we’ve talked about planning for retirement at a high level, as well as specific tips for spending less. But you still need to know specifically what to do with your unspent money, and that’s what this article is all about!

To start with, we’ll talk about where you should put your money, in order of “most important” to “least important”, whether that’s toward debt, savings accounts, or 401(k)s and IRAs. Then after that, we’ll go into more depth about what all of those words actually mean!

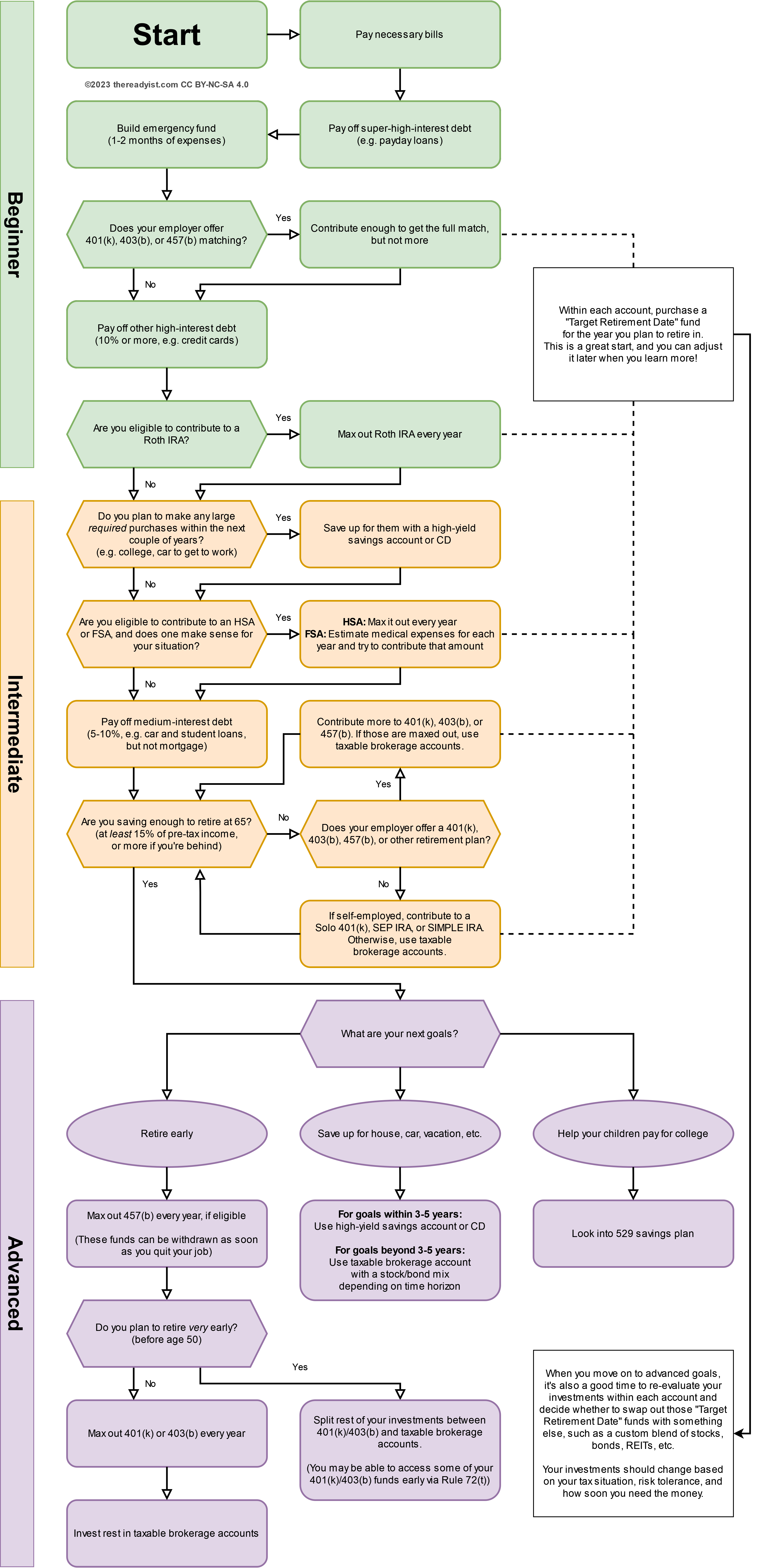

Where to put your money first

Honestly, Reddit has already done a great job here. The Personal Finance subreddit wiki is a fantastic resource, and for the most part, I agree with its recommendations (with a few minor differences here and there).

In particular, their flowchart is an excellent visual way to determine where all of your incoming money should go, and in which order. However, I have a few qualms with some of the specifics of how it orders things, so I went ahead and made my own flowchart! Feel free to share it too, just please link back to here. 🙂

Disclaimer: this is a general guide! While it’s probably “good enough” for most of the population, everyone’s situation is different, so a single guide won’t be 100% optimal for anyone. If you really want to make sure you’re always making the absolute best decisions, you’ll want to book a consultation with a financial advisor—specifically, one that’s a “fiduciary”, meaning that they are legally required to give you good advice and not just sell you whatever makes them the highest commissions.

So with that out of the way, let’s get started on fleshing out the instructions shown in the chart!

Beginner

Pretty much everyone should follow these steps. Even if you don’t have the time or energy to figure out everything right now, these steps are usually considered “no-brainers” and will set you up for success later without tons of effort. I recommend attempting all of these steps ASAP.

Pay off super-high-interest debt

By “super high interest”, I generally mean payday loans, since they can have interest rates of 100%, 500%, or even more! If you have multiple, pay off the ones with the highest interest rate first.

But why does paying these off come before any sort of investing or saving? It’s simple: paying back a loan is a guaranteed return on investment. For comparison, suppose if you had bought a $100 investment with a 10% interest rate. You would make a $10 profit after one year. Debt works the same way, but in reverse—you’d have made a $10 loss. But if you pay off the debt, then you no longer have to pay that interest, which means you are no longer losing that $10. As it turns out, “not losing $10” and “gaining $10” are equally good decisions!

And guess what? You are never going to find any investments with a guaranteed return higher than 100-500%. Not even close! So getting rid of those payday loans first is always the way to go.

Build an emergency fund

As mentioned above, an emergency fund is simply money you keep in a regular bank account (or under your mattress) to pay for necessary emergency expenses, such as car repairs. The reason why you want one is so that you can afford sudden expenses without taking on more debt, like payday loans or credit card debt. Debt weighs you down with interest and minimum payments, but your emergency fund allows you to “borrow from yourself” instead, with no fees whatsoever.

It’s recommended for a basic emergency fund to hold 1-2 months worth of expenses. Some folks like to keep it in a high-interest savings account, such as one offered from CapitalOne or Ally Bank (currently offering rates of about 3.5%, compared to most big banks offering 0.01%). Others like to store some of it in their checking account so that they can leave their bills on autopay without worrying about overdrafting. It’s also not a bad idea to have at least a few hundred dollars worth of cash (preferably in smaller bills like $5s and $20s) hidden somewhere in your home in case of a natural disaster, power outage, etc.

Just remember: don’t use the money unless you really need it! The emergency fund is an alternative to taking out debt. It’s not your fun money!

Should an emergency fund actually be your first step?

Some people think an emergency fund should be your absolute first priority after paying off your necessary bills for the month.

The reason why I recommend paying off payday loans first is because that has a guaranteed high return on investment. If you don’t pay them off quickly, it will definitely cost you a lot in interest payments. Emergencies, on the other hand, are not guaranteed to happen. If you don’t have an emergency, then you may have wasted hundreds of dollars paying extra interest on your debts.

But what if you do have an emergency? Well, then presumably you can just get another payday loan! So even in the worst case scenario, you’re no worse off than where you started. And in the best case scenario, you saved money!

Contribute to 401(k) to get employer match

Many employers offer retirement plans for their employees, such as a 401(k) (for private companies) or 403(b)/457(b) (for nonprofits/governments). These are kind of like bank accounts, except instead of money, they can hold investments too, like stocks and bonds. This is great because those investments can grow over time—WAY faster than a bank account would grow. The catch is that you can’t withdraw the money until you reach retirement age (generally your mid to late 50s). More details on these later.

Some employers offer matching as an extra employee benefit. If your employer offers matching, then for every dollar you contribute to your account, your employer will contribute another. So for example, if you contribute $50, they will contribute $50 too. That’s a guaranteed 100% return on investment—it’s like free money!

Usually they only match up to a certain limit though, e.g. up to 4% of your salary. At this point, you should only contribute enough to get the match, but no more or less!

What to invest in

When you first contribute money to a 401(k), it just sits there earning almost nothing, just like a bank account. If you want it to grow, you’ll need to purchase an investment within the account! For beginners, I generally recommend purchasing a “target retirement date” fund for the year that you plan to retire in. Sometimes these funds go by other names, like “lifestyle” funds. These funds will automatically give you a good blend of stocks and bonds that adjusts automatically over your lifetime, so they’re both easy as well as pretty close to mathematically-optimal in many cases! And you can always revisit this decision later once you get more financial knowledge, and swap out your investments for different ones.

You may wish to do this before building an emergency fund

It depends on your cash flow and what your loan options are.

The main concern here is that without an emergency fund, you might be left needing to take on debt if an emergency occurs. If your only option is to then take out a payday loan at 500% interest, then you might end up paying more in interest than you received from your employer’s 401(k) match. In that case, just keeping the money in your emergency fund would have been smarter.

But if you would be able to pay off the loan in full really quickly (e.g. on your next paycheck), or if you have access to other forms of loans (such as credit cards) with lower interest rates, then you could still come out ahead even after paying a little bit of interest. The employee match might be big enough to cancel it out!

Pay off other high-interest debt (10% or higher)

This includes most credit card debt. Again, it’s important to pay this off because it’s a guaranteed 10%+ return on investment. You’re never going to find that in any other sort of investment, like stocks, bonds, or real estate.

Snowball vs Avalanche

But what should you do if you have multiple debts? Which should you pay off first? There are 2 common strategies:

- Debt Snowball: Pay off your smallest loans first.

- You reduce the number of debts you have to deal with.

- Saves effort (fewer bills to pay)

- Extra cash flow in your budget (fewer minimum payments to make)

- You get a motivational boost every time you fully pay off a loan.

- You reduce the number of debts you have to deal with.

- Debt Avalanche: Pay off your highest-interest loans first.

- You end up paying less interest overall, which is more mathematically optimal.

So then which should you choose? Well, whichever one helps you sleep better! Personally, I prefer the Avalanche method because it’s more mathematically optimal. But others might prefer the snowball method for its stress-reducing and motivational benefits.

Fund a Roth IRA

An IRA is like a 401(k), except it’s not associated with your employer. You can open an IRA account with any financial services company you want, such as Vanguard or Fidelity. We’ll get into the specifics later, but for now, suffice it to say that an IRA is one of the best retirement accounts available, and you’ll definitely want one.

There are 2 main types of IRAs: Traditional IRAs and Roth IRAs. Again, we’ll get into the specifics later, but for most people, I recommend a Roth IRA, largely because you are actually allowed to withdraw the money you put in whenever you want, not just during retirement! This can act as a “backup” emergency fund.

But before you contribute to either kind, make sure you’re eligible! We’ll go over the rules and requirements for contributing to IRAs later. TODO

What to invest in

As mentioned in the 401(k) matching step above, I usually recommend purchasing a “target retirement date” fund within the account. Just make sure it has low fees, e.g. an expense ratio of 0.2% or less.

Why does the Roth IRA step come so early?

Some people (and the Reddit flowchart) recommend increasing the size of your emergency fund before contributing to a Roth IRA, but as I mentioned, a Roth IRA already functions as a backup emergency fund, and it will generally give you a much better interest rate than a bank account will. I and many others don’t think you really need a giant emergency fund. Just note that if you decide to use a traditional IRA instead of a Roth IRA, you actually should increase the size of your emergency fund first, since you can’t withdraw your traditional IRA contributions early without a penalty.

The Reddit flowchart also recommends paying off medium-interest debt (5-10%) before funding an IRA as well, but I also disagree with this. Their reasoning is probably because paying down the debt is a guaranteed 5-10% return on investment, while the investments in an IRA are not guaranteed to grow that fast (even though it’s in the right ballpark for average gains in the long term). But using an IRA reduces your taxes by a known amount, and that amount is guaranteed (at least until tax laws change). For example, if you contribute $1000 to a traditional IRA, then you could get hundreds of dollars in tax benefits! And that’s on top of whatever growth you get on the investments in the IRA.

“Backdoor” Roth IRA

If you make too much money to contribute to a Roth IRA directly (about $129k-144k per year for single tax filers in 2023), there’s another way to contribute called the Backdoor Roth IRA. It’s simply a method to contribute to a Roth IRA indirectly that you can do if you meet certain requirements and are willing to perform a couple extra steps.

Intermediate

Most of these steps aren’t urgent, so if you’re currently overwhelmed with life, feel free to revisit these a bit later. But it’s still best to do them within a couple years!

Save up for large required purchases

If you know you will have some big required expenses coming up in the next couple years, such as college, professional certifications, or getting a car in order to commute to work, then save up for them! Because the stock market can be volatile and you need the money soon, it’s best to keep it somewhere safe, such as in high-yield savings accounts (at least 2-3% interest), CDs, or US bonds.

Note that down payments for a house do not count, since owning your own home is not a requirement (nor necessarily even a good investment). You should focus on the next few steps first. We’ll save for optional large expenses later!

Consider funding an HSA or FSA (if eligible)

An HSA, or Health Savings Account, is similar to a 401(k) or IRA, except that you can also withdraw the money early to pay for medical expenses. The main benefit of them is that they are treated extremely favorably by the US tax system, so using one can potentially save you hundreds of dollars per year in taxes. And if you end up not having very many medical expenses, it eventually just turns into a regular retirement account!

The main downside though is that in order to open and contribute to one, you need to have a specific type of health insurance plan called an HDHP (High-Deductible Health Plan). If you don’t have one of these, then you can skip this step!

If you’d like to learn more about HSAs, check out this article.

What to invest in

As mentioned in the Roth IRA step and the 401(k) matching step above, I usually recommend purchasing a “target retirement date” fund within the account.

FSAs

An FSA, or Flexible Spending Account, is similar to an HSA in terms of tax benefits, but has a few other differences:

- It doesn’t require any particular health plan

- It’s tied to your employer, so you lose the money if you leave your job

- The funds usually expire at the end of each calendar year

- The funds cannot be invested and grow over time

For these reasons, FSAs are usually considered to be worse than HSAs, so if you have to choose between them, an HSA is usually a better option. But if you don’t have access to an HSA, an FSA can still be used to save money on healthcare expenses. You just want to make sure you actually use the money you contribute! For example, if you know you will spend $600 each year on prescription refills (e.g. a $50 monthly copay), then by all means, contribute $600 to your FSA each year. And since you didn’t need to pay income tax on that money, you may have saved hundreds of dollars! Just try not to leave extra money sitting in the account, since you might just lose it.

Pay off medium-interest debt (5-10%)

This can include car loans and student loans, but we’ll skip mortgage payments for now (in case you already own a house). The reason why we want to pay these off before investing further is because investments usually aren’t going to give you a guaranteed return higher than 5%. Plus, paying off these debts will decrease the number of monthly payments you need to make, which makes it easier to weather a potential financial emergency.

But why not pay off my mortgage?

The reason why we are not counting mortgage payments here is because it will likely take a very long time (potentially decades) to pay off your mortgage, and you don’t want to put off investing for that long. This is because over the course of decades, the volatility of the stock market is averaged out, and you’ll actually start seeing your stock market returns consistently beat your mortgage interest rate (in most cases). If your stock market returns grow faster than your mortgage interest accrues, then you’re making money!

Pay off your mortgage as slowly as possible.

Making extra payments on your mortgage can also lead to being “house rich, but cash poor”. If the economy takes a turn and you get laid off, you can’t pay your bills with house equity (and good luck taking out a second mortgage during a financial crisis). Not only will you be unable to buy food and other necessities, but if you can’t make those mortgage and property tax payments, you might even get foreclosed upon, regardless of how much extra you paid earlier.

You can’t eat your house.

So instead of tying up all your money in home equity, just make the minimum mortgage payments and put the bulk of your cash toward more liquid assets instead, such as stocks and bonds in your Roth IRA. That way, you can just sell off your investments for a few months to pay the bills until you get another job.

But what if you’re worried that those stocks might go down right when you need them most, like if you lost your job in a market downturn? Well if your mortgage interest rate is low enough, e.g. 3%, then you could even get guaranteed returns higher than that in some high-yield savings accounts and CDs. You do have to pay taxes on that, but it’s still possible for many to get tax-adjusted guaranteed returns higher than their mortgage interest rate. If that’s the case for you, then paying off your mortgage early is literally throwing money away!

But what if I want to pay off my mortgage early?

Some people prefer to pay it off early because they simply don’t like being in any sort of debt, and getting rid of a mortgage lifts a weight off of their mind. Others are skeptical that investment returns will beat their mortgage interest rate (especially if it’s high, e.g. >6%… you might want to look into refinancing). So if it seems worth it to you, you are obviously allowed to pay off your mortgage early. Ultimately, you have to do whatever helps you sleep at night, regardless of what’s statistically optimal!

Make sure you’re saving enough to retire at 65

Between your 401(k)/403(b)/457(b), IRA(s), and HSA contributions, are you currently saving enough for “regular” retirement at around age 65? Do the calculations from our previous article to figure out your retirement goal. Then open this calculator and enter:

- How many years until your retirement

- How much money you already have saved

- How much you’re currently contributing every month/year

Is the “Average Resulting Balance” above your goal? Ideally in at least 90% of cases (since it tests against historical stock market data to estimate growth)? If so, great!

But if not, then now’s the time to start contributing more to your 401(k), 403(b), and/or 457(b) if you have access to one (and if you’re self-employed, you may want to look into setting up a Solo 401(k), SEP IRA, or SIMPLE IRA).

However, if you don’t have access to a workplace retirement plan, or if you’re already contributing the yearly maximum, then you can invest the rest in taxable brokerage accounts. These are similar to 401(k)s and IRAs in that they can hold investments like stocks and bonds, but they have different tax rules associated. The main upsides are that there are no eligibility requirements, yearly contribution limits, or early withdrawal penalties! We’ll go over more of the details further down. TODO LINK

Advanced

By now, you should be fully on track for retirement. Congratulations! You have a few more options now, based on what your goals are.

Help your children pay for college

You may wish to look into a 529 Plan, another tax-advantaged savings program designed to help pay for college costs. They can even be used to cover costs related to K-12 schools and apprenticeship programs, too!

Save up for a large expense

This can be the down payment on a home, a fancy new car, a dream vacation, whatever!

Similar to the above step to save for large required purchases, it’s generally recommended to keep the money for soon-ish upcoming purchases (e.g. 3-5 years) somewhere safe, such as in high-yield savings accounts (at least 2-3% interest), CDs, or US bonds.

For goals beyond 3-5 years though, the returns of investments like stocks start becoming more reliable, so it’s usually a good idea to invest in riskier stuff like stocks or corporate bonds. A taxable brokerage account should usually be sufficient for this purpose.

Retire early

If you’re already on track for “regular” retirement, then that means you can start focusing on early retirement! If you are eligible for a 457(b) plan through your employer, I generally recommend maxing that out every year if you can, because the money in 457(b) accounts can be withdrawn as soon as you quit that job (or otherwise cease to be employed there).

After that, my recommendations change based on how early you plan to retire. For reference, here’s the timeline of which funds become available (without penalties) to you at different ages:

- Any time: Roth IRA contributions

- Age 55: Roth IRA growth, as well as all Traditional IRA funds

- Age 59.5: 401(k)s and 403(b)s, as well as 457(b)s if you haven’t quit your job yet

- Age 62: You can start taking “early” Social Security payments (at a reduced amount)

- Age 65: HSAs (or you can withdraw any time for healthcare-specific expenses)

- Age 67: You can start taking “normal” Social Security payments (at the regular amount)

- Age 70: You can start taking “late” Social Security payments (at an increased amount)

As you can see, the later you retire, the more money you have available to you. If you tried to retire at, say, 50, you might have a hard time because you wouldn’t be able to withdraw any of your retirement funds without taking a 10% penalty (with the exception of Roth IRA contributions, which you can always withdraw). But you might be able to retire at age 55… as long as you’re able to live off of your IRA until your 401(k) kicks in after 4.5 years.

Note that there are technically ways to get money out of your 401(k) early. For example, you could just pay the 10% penalty. Or you could take out a 401(k) loan, or begin SEPP distributions via Rule 72(t). There’s even an obscure loophole called a Roth Conversion Ladder. But there’s no guarantee that these options will work for you (or even exist) by the time you retire, so if you want to retire really early (like before 50), then you’ll probably want to store some money outside of retirement accounts.

This is where taxable brokerage accounts come in! As mentioned earlier, these are similar to 401(k)s and IRAs in that they can hold investments like stocks and bonds, but they have different tax rules associated. The main upsides are that there are no eligibility requirements, yearly contribution limits, or early withdrawal penalties! In fact, there isn’t even a concept of “early” withdrawal—it works just like a bank account. Your money is your money, and there are basically no restrictions on what you can do with it. So if you want to retire before the rest of your regular retirement accounts become available, you’ll most likely want to have some of your money in taxable brokerage accounts!

We’ll go over more of the details on taxable brokerage accounts further down. TODO LINK. But for now, basically all you need to know is that the earlier you plan to retire, the more of your funds you should probably allocate to taxable brokerage accounts. For example, if you plan to retire at 45 here’s how you might plan your retirement:

- Age 45-54: live off of brokerage account until empty, then Roth IRA contributions

- Age 55-59.4: live off of Roth IRA growth

- Age 59.5 and beyond: live off your 401(k)/403(b)

If you suppose that you need $40k per year to live, then a conservative estimate would say that you need 10 x $40k = $400k during that first 10 years of retirement. You might have, say, $150k of contributions to your Roth IRA, so that means you would need $250k worth of investments in a taxable brokerage account in order to add up to $400k.

Then for the second portion of retirement, that $150k of Roth IRA contributions will probably have grown to around $400k by the start of your retirement, which means you have another $250k to live off of for 5 years. Should be more than enough!

Finally, for the last portion, we can figure out how much we’ll need in our 401(k) by using the 4% Rule that we discussed in the last article. To refresh your memory, the 4% Rule states that if you have a million dollars, you can withdraw $40,000 every year, forever, and chances are that you will never run out of money. That means that the total amount of money we need for retirement will be about 1 million dollars! Since we already had $250k in taxable brokerage accounts and $400k in a Roth IRA, that means we only need about $350k in our 401(k) at the start of our retirement.

But wait, if we burned through $400k in just our first 10 years of retirement, how on earth is a $350k 401(k) going to last forever? Well that’s where investments and the 4% rule come in! When we withdraw that first $40k (i.e. 4%) at the start of retirement, the other $960k is still growing in the stock market! And since it’s usually pretty easy to get at least 4% returns every year, that means that you get another $40k to replace the chunk you just lost. Infinite money! You’re just “living off the interest”!

You may realize though that since the brokerage account is only worth $250k, it might only grow by $10k per year, all while you’re withdrawing $40k per year. This means that your brokerage account will eventually get emptied out. But at the same time, your other accounts are growing freely! So during your retirement, your wealth is essentially being shifted between accounts over time, even while your total amount of wealth is staying roughly the same.

Conclusion

If you’ve made it this far, congratulations! I’m sure it wasn’t an easy journey. Just remember, again, this article is just a general guide, and may not be 100% optimal for you. But if you’re just getting started, it’s a great starting point, and will most likely be “good enough” for you for years. But you should never stop learning, so eventually, I expect most folks to eventually branch off and do whatever makes the most sense for their own lives. So good luck to all of you lifelong learners!

Speaking of learning, I used a lot of complicated words in this article! I may have briefly mentioned what a 401(k) or Roth IRA was, but I haven’t yet gone into depth. So if you’ve gotten to a step where I used concepts that you don’t fully understand, I highly recommend looking them up to make sure you at least know the basics! Luckily, for most of them, I’ve written a whole separate article that goes over most of the common terms you’ll see when it comes to retirement:

TODO LINK

{kind=link}

One thought on “What to Do With Your Money: The Big Flowchart”